Home › Market News › Bitcoin, Natural Gas, and Stock Sector Allocations

The Economic Calendar:

MONDAY: Chicago Fed National Activity Index (7:30a CT), Dallas Fed Manufacturing Index (9:30a CT), 2-Year Note Auction (12:00p CT)

TUESDAY: Building Permits (7:00a CT), Redbook (7:55a CT), House Price Index (8:00a CT), CB Consumer Confidence (9:00a CT), New Home Sales (9:00a CT), Richmond Fed Manufacturing Index (9:00a CT), Dallas Fed Services Index (9:30a CT), Money Supply (10:00a CT), 5-Year Note Auction (12:00p CT), FOMC Minutes (1:00p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), PCE (7:30a CT), Corporate Profits (7:30a CT), Durable Goods (7:30a CT), U.S. GDP (7:30a CT), Jobless Claims (7:30a CT), Retail Inventories (7:30a CT), Wholesale Inventories (7:30a CT), Chicago PMI (8:45a CT), Pending Home Sales (9:00a CT), EIA Petroleum Status Report (9:30a CT), 7-Year Note Auction (10:30a CT), EIA Natural Gas Report (11:00a CT), Baker Hughes Rig Count (12:00p CT)

THURSDAY: U.S. Holiday – Thanksgiving

FRIDAY: Fed Balance Sheet (3:30p CT)

Key Events:

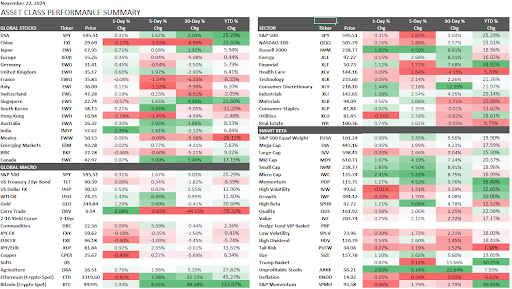

Bitcoin’s recent surge has been nothing short of spectacular. With a spot new all-time high of $99,800 last week, its monthly performance has skyrocketed to an astonishing +41%. This far outpaces traditional safe-haven assets like gold (+5.3%) and silver (+8.0%).

The crypto market’s overall growth, fueled by a favorable regulatory climate under the incoming Trump administration, has seen its capitalization soar from $2.5 trillion to $3.5 trillion. Bitcoin’s market cap has expanded to a staggering $1.796 trillion, surpassing both silver and Saudi Aramco. This positions Bitcoin as one of the world’s largest assets.

Fed Fund futures are trading at a 52% probability of a 25 basis point rate cut at the next FOMC meeting, which is scheduled for December 18.

The market is currently pricing a stall in Fed Fund rate cuts in the 4.25-4.5% range until May.

The stock market ended the week positively, with the S&P 500 registering a gain of 1.6% and the Nasdaq 100 advancing by 1.8%.

Market Sentiment:

Sector Rotation:

Here’s a snapshot of how hedge and mutual funds allocate to sectors compared to the Russell 3000 index.

Volatility at its best. The past 18 months have been a rollercoaster ride for SFR8, with multiple 100+ basis point swings in both directions.

Despite this extreme volatility, the year double fly has paradoxically narrowed. This suggests a significant increase in algorithmic trading activity this year. These algorithms are exploiting the market’s wild swings, leading to trading patterns that deviate from historical norms.

Many traders believe this is NOT how the double fly “should” trade with respect to major rate-level changes. Traders have to adapt to the new environment!!!

Oil markets are experiencing a tug-of-war. Increasing geopolitical risks are pushing prices upward, while a strengthening dollar, which has hit new peaks, is dampening the potential for an oil price surge driven by war-related risks.

The market is grappling with the notion that President Biden might be inclined to intensify global tensions as his term winds down. This sentiment appears to be influencing perceptions of risk not only with Russia but also with Iran:

Iran’s Nuclear Activities: Initially, there was a market sell-off when headlines suggested Iran might halt its pursuit of weapons-grade uranium. However, these reports were misleading. Recent developments have provided clarity that Iran has declared intentions to ramp up its nuclear fuel production capacity.

This decision comes in the wake of a censure from the United Nations’ atomic watchdog, escalating tensions with Western nations. According to Bloomberg, Mohammad Eslami, head of Iran’s Atomic Energy Organization, has called for the deployment of a “significant collection” of “new and advanced” centrifuges. This move is in direct response to the International Atomic Energy Agency’s criticism over unresolved investigations into uranium particles at unreported locations, as announced by Iran’s Foreign Ministry.

Euro FX futures experienced a significant decline on Friday, reaching $1.035, the lowest since November 2022. This drop came in the wake of the latest PMI data, which highlighted continued economic fragility within the Euro Zone.

Business activity has shown signs of weakness, prompting traders to speculate on a potential further depreciation of the Euro, potentially reaching parity with the U.S. Dollar. This rare occurrence has only been observed twice since the Euro’s inception in 1999.

Traders have noted that the Euro’s weakness could be attributed to both internal economic challenges and external pressures, such as a strong U.S. economic performance and anticipated policy divergence between the ECB and the Federal Reserve.

A sudden cold snap boosted the natural gas markets this week. However, the market traded much lower on Friday as traders took profits. In the short term, key support is around the $3 level.

Early last week, the anticipation of cold weather led to a spike in natural gas futures, with traders positioning for increased heating demand. Should these forecasts for a very cold December materialize, we might witness a sharp rise in natural gas prices due to heightened consumption for residential and commercial heating purposes.

Some weather forecasters are now predicting that December might turn out to be unusually cold, which, if realized, could significantly alter market dynamics for diesel, heating oil, and natural gas.