Home › Market News › FOMC, BOE & BOJ Rate Decisions All This Week

The Economic Calendar:

MONDAY: Empire State Manufacturing Index (7:30a CT), NOPA Crush Report (11:00a CT)

TUESDAY: Retail Sales (7:30a CT), Redbook (7:55a CT), Industrial Production/Capacity Utilization (8:15a CT), Manufacturing Production (8:15a CT), Business Inventories (9:00a CT), Fed Logan Speech (9:00a CT), HAHB Housing Market Index (9:00a CT), Retail Inventories (9:00a CT), 20-Year Bond Auction (12:00p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), Building Permits (7:30a CT), Housing Starts (7:30a CT), EIA Petroleum Status Report (9:30a CT), FOMC Announcement (1:00p CT), Fed Chair Press Conference (1:30p CT), Overall Net Capital Flows (3:00p CT)

THURSDAY: Jobless Claims (7:30a CT), Philly Fed Manufacturing Index (7:30a CT), Existing Home Sales (7:30a CT), EIA Natural Gas Report (9:30a CT)

FRIDAY: Baker Hughes Rig Count (12:00p CT), Fed Harker Speech (7:30a CT)

Key Events:

The Federal Reserve is anticipated to lower interest rates by 25 basis points at Wednesday’s upcoming policy meeting.

The market is pricing in a 50/50 probability of a 25 or 50 basis point rate cut.

This decision aims to achieve a soft landing for the economy, particularly in light of the disappointing July jobs report.

The Federal Reserve is poised to implement its first interest rate cut since 2020. While a 25-basis-point cut is widely expected, a larger 50-basis-point cut remains a possibility.

Lower interest rates in the U.S. will have global implications. A new easing cycle by the Fed will narrow the rate differentials between central banks worldwide.

The recent CPI data has reduced the odds of a more aggressive rate cut.

Bank of America forecasts a series of 25-basis-point cuts through March 2025.

Recent comments from influential former Fed official Bill Dudley have shifted expectations, making a 50-basis-point cut more likely. The market is now evenly divided on the potential size of the rate cut.

Source: CME Fedwatch

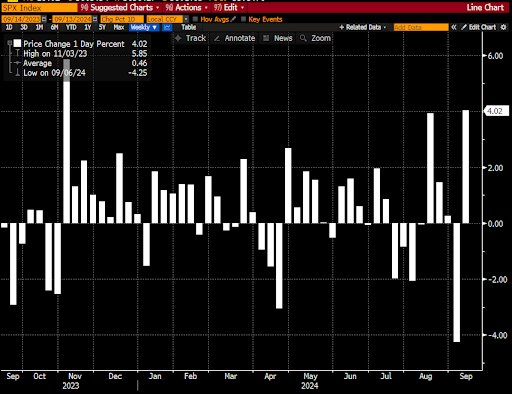

Last week, the stock market experienced a dramatic turnaround. After a volatile start marked by concerns about economic growth and inflation, the market rallied strongly towards the end of the week.

The S&P 500 and Nasdaq 100 closed the week with gains of +4.01% and +5.94%, fully recovering from losses earlier in the week. Positive economic data and growing expectations for a Federal Reserve rate cut fueled this reversal.

Inflation data, employment reports, and investor sentiment regarding the Federal Reserve’s monetary policy are all key factors influencing the market.

It’s worth noting that the previous week was the worst week for the S&P 500 in 2024. However, this past week marked a significant reversal, with the S&P 500 reaching near-all-time highs despite previous downward pressure.

Given the recent rally and the anticipated rate cut, the S&P 500 could make further gains. Some analysts predict the index could reach 6,000 by December.

Source: Bloomberg

The Bank of Japan (BoJ) is expected to maintain its current monetary policy stance at its meeting.

The BOJ has consistently signaled a gradual approach to policy rate hikes.

While there has been speculation about a potential shift in policy, given the recent global economic trends and the yen’s weakening, the consensus among analysts is that the BoJ will likely keep interest rates unchanged.

Source: TradingView

The current state of the oil market, characterized by low prices and supply/demand imbalances, is raising concerns about the global economy.

While optimists view this as a potential precursor to a soft landing and a reduction in inflation, the market’s behavior suggests a more pessimistic outlook.

The disconnect between futures prices and the physical market is puzzling, given the low oil prices and refiners’ willingness to pay a premium for crude. This discrepancy could be attributed to a market perception of an impending economic downturn or a belief that peak demand has been reached.

The sentiment surrounding oil is worse than during the global financial crisis, the European sovereign debt crisis, or the COVID-19 lockdowns.

The question remains: Are the economic conditions truly as dire as the market suggests? Hedge funds and other market participants will likely assess these factors and decide based on their analysis.

Source: TradingView

The U.S. natural gas market has grappled with a supply surplus driven by mild winters and increased production. Despite a surge in demand due to this summer’s heat and the temporary shutdown of LNG exports caused by Hurricane Beryl, the overall supply glut has kept prices low.

Front-month Henry Hub prices have averaged $2.19 per million British thermal units (MMBtu) this year, the lowest average since the pandemic-era demand shock in 2020.

While increased demand from natural gas-fired electricity generation helped offset some of the surpluses, Hurricane Beryl’s impact and limited growth in LNG exports have constrained price increases.

Natural gas prices are expected to remain under pressure in the near term. The upcoming startup of the Matterhorn pipeline will alleviate regional supply gluts but add to overall supply. Additionally, the high price spread between October and December contracts incentivizes producers to delay production and sell forward contracts, potentially leading to a surge in production later this year.

Looking ahead, the next significant boost to natural gas demand is not expected until 2026, when additional LNG export capacity is scheduled to come online.

Source: TradingView

Spot Bitcoin ETFs have experienced their longest net outflows since their launch earlier this year, with nearly $1.2 billion withdrawn over eight days ending September 6th.

This trend is attributed to global economic concerns, including mixed U.S. job data and deflationary pressures from China.

Bitcoin prices can be characterized by brief periods of upward momentum followed by sharp declines.

While ETFs were initially buying over 4,000 Bitcoins per day, this rate has plummeted to zero on multiple occasions.

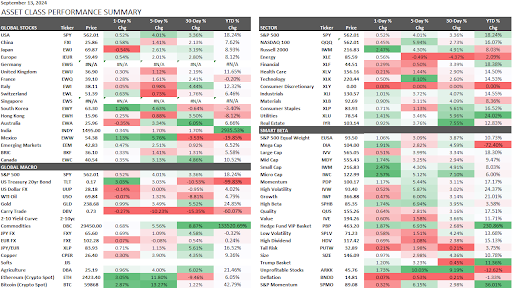

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.