Home › Market News › Free Market Profile and Auction Theory Class!

The Economic Calendar:

MONDAY: Leading Indicators, 3-Month Bill Auction, 6-Month Bill Auction

TUESDAY: PMI Composite Flash, Richmond Fed Manufacturing Index, 52-Week Bill Auction, 2-Yr Note Auction, Money Supply

WEDNESDAY: MBA Mortgage Applications, State Street Investor Confidence Index, EIA Petroleum Status Report, Survey of Business Uncertainty, 4-Month Bill Auction, 2-Yr FRN Note Auction, 5-Yr Note Auction

THURSDAY: Durable Goods Orders, GDP, International Trade in Goods, Jobless Claims, Chicago Fed National Activity Index, Retail Inventories, Wholesale Inventories, New Home Sales, EIA Natural Gas Report, Kansas City Fed Manufacturing Index, 4-Week Bill Auction, 8-Week Bill Auction, 7-Yr Note Auction, Fed Balance Sheet

FRIDAY: Personal Income and Outlays, Consumer Sentiment, Pending Home Sales Index, Baker Hughes Rig Count

Futures Expiration and Rolls This Week:

WEDNESDAY: Natural Gas futures roll from February (G) to March (H)

THURSDAY: Gold futures roll from February (G) to April (J)

Key Events:

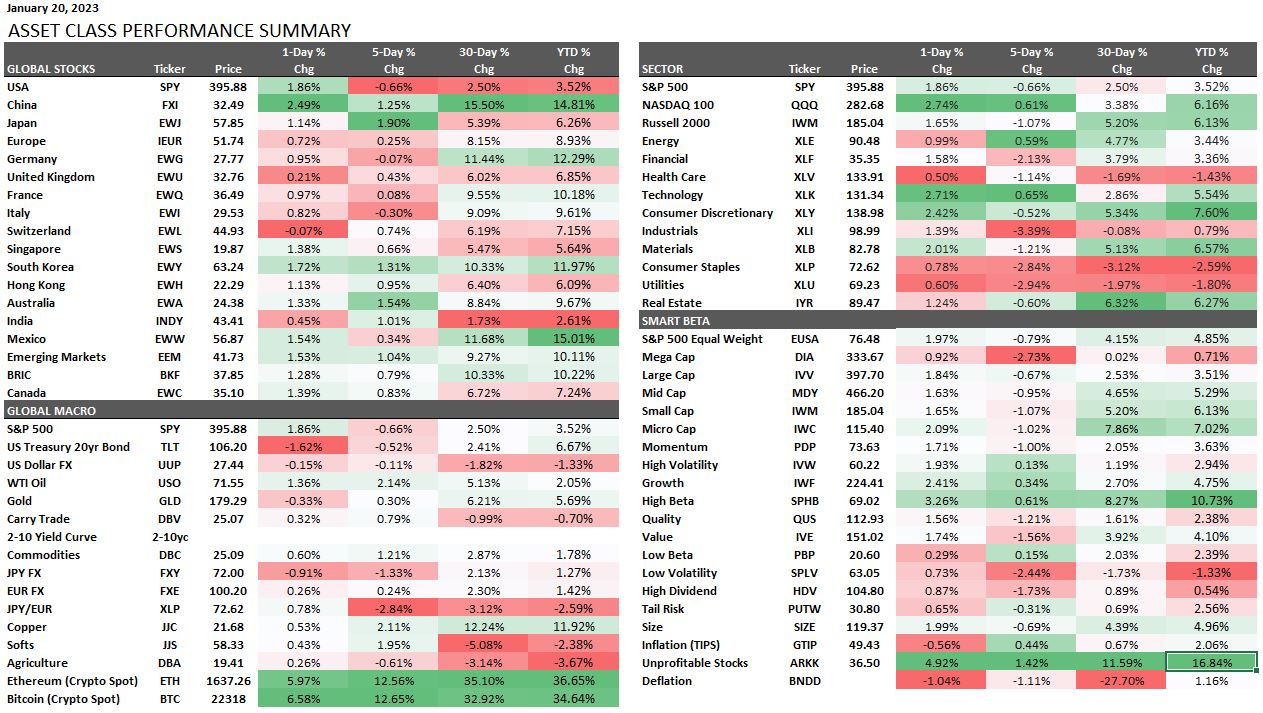

Stocks mounted a significant comeback on Friday to finish a mixed week of returns. The S&P 500 was lower on the week by -0.66%, and the Nasdaq 100 was higher by +0.61%.

High beta mid and small-cap stocks have been the return leaders in 2023.

The U.S.Tech sector stocks are off to a strong start this year, but not because Q4 earnings reports will be especially impressive. Instead, the market hopes that all the bad news about Q4 & forward earnings guidance is already baked into the stock price.

David Kostin, the chief US equity strategist for Goldman Sachs, points out that the current 3-month trend of S&P 500 forward EPS revision sentiment is the most negative reading outside of the 2008 and 2020 recessions – suggesting a hard landing is still a real possibility.

Marko Kolanovic, Chief Market Strategist at J.P Morgan, fears a recession and central bank over-tightening. As a result, J.P. Morgan sees downside risk for the stock market in the first quarter of 2023.

Although inflation in the U.S. is easing, Kolanovic said, “the market is behaving as if we were in an early cycle recovery phase, but the Fed has not even concluded hiking yet.”

Decoded. He refers to one of the four distinct business cycle phases. After a “recession” comes the “early cycle,” typically when economic indicators start to turn more positive, assisted by more credit and low-interest rates, which aid profit growth. Business inventories are low, and sales grow significantly. It’s in this period that equities tend to see their best performance in the entire business cycle.

Even though many Fed heads are pushing back on the idea of rate cuts in 2023, the fed fund futures curve was pricing in massive rate cuts through March of 2024 (56 bp current and 67 bp on Wednesday)

On the longer term part of the yield curve, traders are pricing a recession into 10yr Treasury market. Last Wednesday’s move in 10-year yields was dramatic (>16 basis points (bp)). In statistical terms, a 16 bp decline is very close to a three standard deviation move (18 bp). The 10yr yield 200-day moving average is around 3.30%.

Traders no longer see inflation as an essential threat but are more worried about an economic slowdown or recession that brings lower prices.

U.S. Treasury yields current yield compared to the last newsletter:

30-Year yield 3.65% vs. 3.62%

10-Year yield 3.48% vs. 3.51%

5-Year yield 3.56% vs. 3.61%

2-Year yield 4.17% vs. 4.24%

2-10 Yield spread -0.69% vs. -0..73%

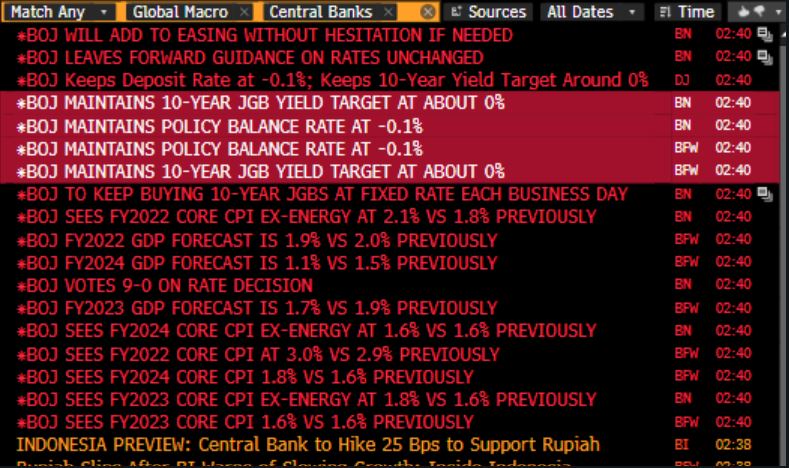

A colossal risk is brewing, and the Western financial press does not see it as an issue. The risk is this: The Bank of Japan is spending tens of billions of dollars worth of yen to enforce BOJ governor Kuroda’s yield curve interest rates suppression program.

The BOJ introduced its policy of yield curve control in the fall of 2016 by keeping the yield on ten-year government bonds within a target range through direct interventions in the bond market.

What’s different this time is that the market price action is on to something. In addition, the Bank of Japan has already lifted the allowable ceiling on ten-year JGB yields to 0.5% from 0.25% at the end of 2022. Add to this that Governor Kuroda’s term is up on April 8.

Despite assurances that yield suppression is here to stay, the market is making it more challenging and expensive to control. So, could this be the end of a regime and a once-in-a-lifetime trade setup?

The current rally in Bitcoin has all the hallmarks of a “FOMO rally,” with many sidelined traders with short or fiat exposure in anticipation of further downside. This has caused a short squeeze and subsequent strength in BTC and ETH. Prices have recovered to November 2022 price levels and the scene of the FTX crime.

We have also heard rumors that the Binance exchange is considering phasing out USDT in favor of its internal BUSD stablecoin. While it went relatively unnoticed, Binance phased out USDC stablecoin recently.

All three stablecoins have different niches in the crypto market — USDT is for trading, USDC is used for Ethereum and DeFi, and BUSD is used on the Binance exchange and Binance Smart Chain.

This quote is valid for commodity and futures traders.