Home › Market News › Grains, Rates, and SOFR Futures

The Economic Calendar:

MONDAY: Consumer Inflation Expectations (10:00a CT), Monthly Budget Statement (1:00p CT)

TUESDAY: NFIB Business Optimism Index (5:00a CT), PPI (7:30a CT), Redbook (7:55a CT), Fed Schmid Speech (9:00a CT), Fed Williams Speech (2:05p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), CPI (7:30a CT), Core Inflation Rate (7:30a CT), Empire State Manufacturing Index (7:30a CT), Fed Barkin Speech (8:20a CT), Fed Kashkari Speech (9:00a CT), EIA Petroleum Status Report (9:30a CT), Fed Williams Speech (10:00a CT), Fed Goolsbee Speech (11:00a CT), NOPA Crush Report (11:00a CT), Beige Book (1:00p CT)

THURSDAY: Jobless Claims (7:30a CT), Import/Export Prices (7:30a CT), Philly Fed Manufacturing Index (7:30a CT), Retail Sales (7:30a CT), Business Inventories (9:00a CT), NAHB Housing Market Index (9:00a CT), Retail Inventories (9:00a CT), Fed Balance Sheet (3:30p CT)

FRIDAY: Building Permits (7:30a CT), Housing Starts (7:30a CT), Industrial Production/Capacity Utilization (8:15a CT), Manufacturing Production (8:15a CT), Baker Hughes Rig Count (12:00p CT), Foreign Bond Investment (3:00p CT)

Key Events:

U.S. CPI Preview: No Relief in Sight for the FOMC.

December’s inflation data is not expected to bring good news for the Federal Reserve. Following the recent positive surprises in the jobs reports last Friday, price growth data will likely show that inflation remained stubbornly high at the end of last year.

While markets anticipate a modest slowdown in core inflation to 0.2% month-over-month in December, this is likely only enough to stabilize headline core price growth at 3.3% year-over-year.

Source: Trading Economics

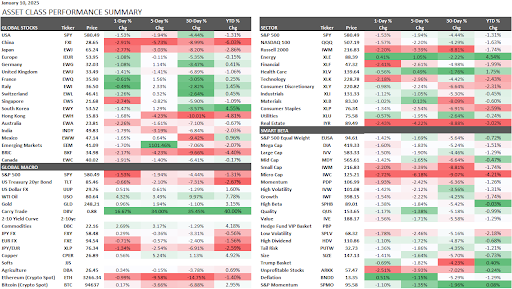

Last week, the S&P 500 fell by -1.94% and the Nasdaq 100 declined by -2.2%

The stock market experienced a significant decline last week, driven by a stronger-than-expected jobs report and hawkish signals from the Federal Reserve. The robust labor market data reinforced expectations of a slower pace of interest rate cuts, prompting a sell-off across major indices.

Despite the recent market downturn, the S&P 500 has delivered strong returns in recent years, achieving consecutive years of positive returns, a feat not seen since the late 1990s. However, this sustained performance has led to elevated valuations, raising concerns among some investors.

Options positioning indicates a lack of fear ahead of the Earnings season despite significant macro equity selling in futures over the past three weeks. Earnings-day moves last quarter were larger than any time in the past 14 years, but options implied moves for the upcoming earnings season are at a six-quarter low.

The 10-year Treasury yield, 4.70% before the Friday jobs report, jumped to 4.78% in its aftermath, up nine basis points from yesterday. The 2-year yield, most sensitive to changes in the fed funds rate, rose from 4.29% just before the report to 4.40%, an increase of 13 basis points from yesterday.

The December US Non-Farm Payrolls report showed an increase of 256,000 jobs, significantly exceeding the forecasted 160,000 and beating the highest Wall Street estimate.

This news fuels speculation that the Federal Reserve might further slow down the pace of rate cuts in 2025. Earnings aligned with expectations, and the unemployment rate slightly decreased to 4.1%. Given the robust labor demand, the Fed will likely opt for an extended pause on rate adjustments for the time being.

Regarding U.S. rates, there’s continued “heaviness” at the long end of the yield curve. This trend is compounded by a strong “Risk-ON” sentiment in the U.S. at the start of the year, alongside market reactions to President-elect Trump’s refutation of a Washington Post story suggesting a possible retreat from earlier tariff commitments.

Source: CME Fedwatch

The market has significantly revised downward its expectations for Federal Reserve rate cuts in 2025. With the economy demonstrating resilience and inflation remaining stubbornly high, the market now anticipates a mere 40 basis points of rate cuts over the next 18 months. This sharp reduction in expected easing reflects a shift in market sentiment towards a more hawkish Fed outlook.

Specifically, fading trades from the recent rise in longer-term interest rates, such as “(back) Red- and Green- SOFR Upside” strategies, offer a compelling risk/reward proposition. These trades can also help hedge against potential losses in equity portfolios. We are using call spreads to structure trade.

Source: TradingView

Source: TradingView

Corn and soybean futures rise on WASDE report and break out of the technical consolidation pattern.

The USDA’s recent World Agricultural Supply and Demand Estimates (WASDE) report sent shockwaves through the grain market, triggering a sharp price increase. The report revealed a significant tightening of grain supplies due to weather-related production issues in the U.S. while simultaneously projecting robust demand.

This unexpected combination of factors, particularly the larger-than-expected supply reduction, caught analysts off guard and fueled a rapid price surge.

Before the release of the WASDE report, weekly export sales data had shown weaker-than-expected figures. However, traders largely overlooked these figures in anticipation of the more comprehensive WASDE report.

Given the tight supply situation for grains, particularly corn, market volatility is expected to persist in the coming months.

Source: TradingView

Source: TradingView

We forecast the market to front load USD strength, then fade in the year’s second half. DXY at 111 (Mar-25), 107 (Dec-25).

Even without tariffs, the Macro backdrop would argue for further USD outperformance, with economists suggesting upside risks to U.S. growth and inflation.

The main risk is that this is a crowded position. The USD is following the 2016/17 playbook well, which was the moment to sell it in 2017 as Trump disappointed on policies.

The Californians affected by the fires are in our thoughts and prayers.

We are monitoring lumber futures with the Palisades Fire Total Damages As High As $150 Billion (AccuWeather estimate). The scope of damage has started to trickle out but is still in the very early stages.

With the new demand for lumber to rebuild California homes, the risk of a potential tariff hike imposed on Canadian exports to the U.S. as early as January will highlight developments that could define first-quarter trends in the softwood lumber market.

Oil and natural gas futures are experiencing significant price increases due to a confluence of bullish market fundamentals and severe weather conditions.

Additionally, the onset of what could be the coldest January in 11 years is heightening demand for heating oil, leading to increased heating oil crack spreads and a global uptick in oil product prices.

Refineries face operational challenges with power outages and the risk of pipeline freezing, while producers are concerned about ice crystals potentially halting hydrocarbon extraction.

Geopolitical tensions are also playing a crucial role in the current market dynamics. There’s been a notable increase in buying from countries like India and China, driven by fears of impending sanctions on oil producers like Iran, Russia, and Venezuela, particularly with the incoming Trump administration. Reports indicate that these countries are stockpiling ahead of potential disruptions in supply due to sanctions on tankers and stricter stances on oil transport.

The surge in oil demand is also influenced by specific trade dynamics, notably with Canada. As reported by Reuters, U.S. crude oil imports from Canada hit record highs last week in anticipation of potential tariffs from the incoming Trump administration. This comes amidst President Trump’s comments about reducing reliance on Canada, focusing solely on oil, which could alter trade relations significantly.

Natural gas prices are similarly affected, with the cold weather posing risks such as freezing gas wells and refineries, which could lead to supply disruptions. The market is preparing for or reacting to these conditions, with prices reflecting the urgency to secure supplies before or during the cold spell.

There is no shame in booking profits and moving to a flat position.

If digital assets can find their footing with the incoming administration, there is still plenty of time to catch the move in BTC to $153k, or $250k, or beyond once it clears the current high of $109k.

Bitcoin has recently tested its November lows without a significant price break, indicating potential strength. While the market remains volatile, there’s no need to panic sell.