Home › Market News › Soybeans, The U.S. Dollar, and SMCI Accounting Shenanigans

The Economic Calendar:

MONDAY: US Labor Day Holiday: Markets Closed

TUESDAY: Redbook (7:55a CT), S&P Global Manufacturing PMI (8:45a CT), Construction Spending (9:00a CT), ISM Manufacturing Index (9:00a CT), Total Vehicle Sales (9:00a CT), 52-Week Bill Auction (12:00p CT)

WEDNESDAY: MBA Mortgage Applications (6:00a CT), Balance of Trade (7:30a CT), Factory Orders (9:00a CT), JOLTs (9:00a CT), Beige Book (1:00p CT)

THURSDAY: Challenger Job Cuts (6:30a CT), ADP Employment Change (7:15a CT), Jobless Claims (7:30a CT), S&P Global Composite PMI (8:45a CT), ISM Services Index (9:00a CT), EIA Natural Gas Report (9:30a CT), EIA Petroleum Status Report (10:00a CT), Fed Balance Sheet (3:30p CT)

FRIDAY: Unemployment Rate (7:30a CT), Baker Hughes Rig Count (12:00p CT)

Key Events:

The upcoming week will bring a flurry of crucial labor market data that will likely shape trader sentiment and influence the Federal Reserve’s monetary policy decisions.

Key Labor Market Indicators:

Implications for the Fed’s Rate Cut:

The July nonfarm payrolls report sent shockwaves through financial markets. The stronger-than-expected job growth raised concerns about the Fed’s ability to combat inflation effectively without triggering a recession.

The upcoming labor market data will play a pivotal role in determining the size of the Federal Reserve’s anticipated rate cut in September.

Source: TradingEconomics

The rapid recovery of market confidence following a recent global sell-off in risky assets has raised concerns among traders.

We are entering a seasonally lousy month for stocks, but the seasonal trends pattern has been mixed lately.

Historically, September has been a challenging month for the stock market, with an average return of -1.7% over the past century. In contrast, the fourth quarter has typically been a strong period, with an average return of +4.2%.

However, the trend has reversed over the last five years. September has seen an average decline of -4.2%, while the fourth quarter has delivered an impressive average return of +9.8%.

The year 2024 has deviated from both the five-year and ten-year seasonal trends. Every month, except for January, has delivered either a surprising direction or magnitude of return, suggesting that market dynamics may be undergoing a significant shift.

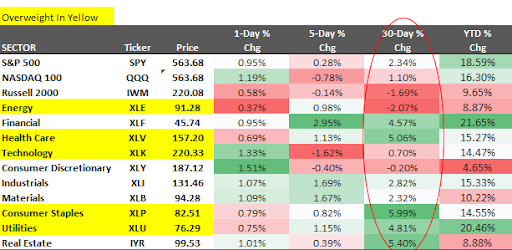

Sectors that outperformed in August were Consumer Staples, Utilities, Healthcare, Financials, and Real Estate.

The laggard sectors were Energy, Technology, and Consumer Discretionary.

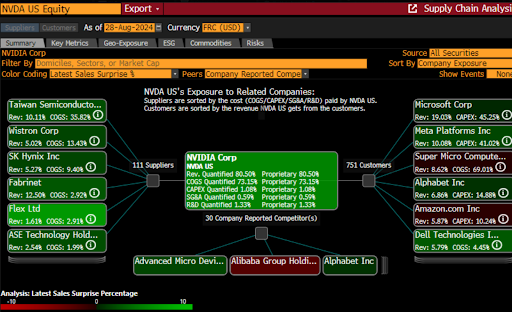

SMCI, a prominent player in the semiconductor industry, has faced significant challenges due to short seller’s allegations of accounting fraud. These accusations, coupled with the delayed filing of its 10-K financial report with the SEC, have cast a dark cloud over the company.

Given SMCI’s position as NVIDIA’s third-largest customer, the company’s financial instability could have far-reaching implications for NVDA, including a potential impact on its revenue and supply chain.

Rumors (stress rumors) have circulated suggesting that NVIDIA may be extending 100% credit to its customers, including startups with substantial cash burn, to facilitate the purchase of GPUs. While these claims remain unverified, they raise questions about NVIDIA’s credit policies and risk management practices.

Soybean futures caught short sellers sleeping last week with a +3.9% gain.

China is slowly playing catch-up on bean purchases. The USDA reported a private export sale of 132,000 metric tons (MT) of soybeans to China and another 100,000 MT of soybean meal to Colombia. These sales provide a positive outlook for soybean demand.

Over the past three years, hedge funds have averaged a net long position of 56,600 soybean contracts. They reached a record net short position over the past few weeks.

Watch for more shorts being squeezed if China continues with more purchases.

Source: Tradingview

Citigroup currency strategists call for the U.S. dollar to rally into the presidential election.

The primary driver of the bank’s bullish outlook is the possibility of a more protectionist trade policy under a second Trump administration.

The U.S. dollar currency heads toward its steepest monthly drop since December.

Source: Tradingview

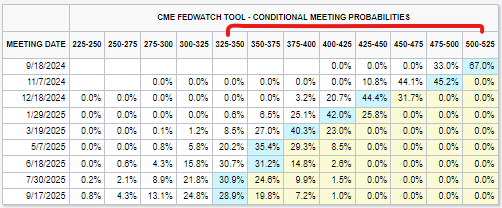

The long-awaited Fed rate cuts are on the horizon. The market expects a 67% chance of a 25 basis point rate cut at the Fed’s next meeting on Sept. 18.

The Federal Reserve has not lowered interest rates for over a year, one of the longest periods without a rate cut since the 1970s. This unprecedented dry spell was only surpassed by June 2006 and September 2007, when it took 15 months to see a rate reduction.

Historically, the average time between the last rate hike and the first cut is eight months. Given that September 2024 marks 14 months since the previous rate increase, a rate cut is highly anticipated.

The Federal Reserve’s decision to maintain high interest rates has been a strategic response to combat inflation. However, as inflationary pressures ease, the central bank is poised to pivot towards a more accommodative monetary policy.

Gavekal Research provides some key takeaways on how the markets could react to each candidate’s victory in November.

These performance charts track the daily, weekly, monthly, and yearly changes of various asset classes, including some of the most popular and liquid markets available to traders.